It might pay to buy into this year's worst-performing sector, according to two traders.

After a middling performance in 2020, consumer staples stocks have kicked off 2021 as the only S&P 500 sector in the red, down more than 3% year to date.

Some of the group's major players including PepsiCo, Tyson Foods, Kellogg and Kraft Heinz reported earnings Thursday morning to a mixed response from equities investors. PepsiCo, Tyson and Kellogg fell, while Kraft Heinz surged after announcing a deal to sell its nuts business to Spam maker Hormel Foods.

Known for their "slow and steady growth," consumer staples stocks have a lot to offer longer-term investors, said Boris Schlossberg, managing director of FX strategy at BK Asset Management

They're no meme stocks, "but if you're looking for very, very safe, secure companies that are going to be around for years and years, that are going to grow at high single digits, I think the whole group is actually an excellent choice," Schlossberg told CNBC's "Trading Nation" on Thursday.

He highlighted PepsiCo, which slid nearly 2% Thursday despite a strong fourth-quarter earnings report. The company beat analyst estimates and told shareholders it expected 2021 growth to meet its long-term goals.

Money Report

"Although the stock is down a little bit today off earnings, it's a stock that has essentially doubled in the last decade, and I think it has every chance of doubling in the next decade," Schlossberg said.

"The key thing here is just simply long-term perspective. It executes very well. It's got a tremendous dominance in the salty snacks business," he said. "It is going to have tremendous growth ... not just in China, but Asia ex-China where I think that kind of food staple is going to be very attractive to the growing middle class. So, I see very good things for PepsiCo."

Schlossberg's other pick was Kraft Heinz, which also topped estimates in its fourth-quarter report.

"It's had tremendous amount of problems but has really been able to steady the ship. Its free cash flow now is over $5 billion and the stock now has certainly put in a very solid foundation, so it has every chance to go to maybe around $50 a share over the next three to five years," he said. "The key thing with all of these stocks is that you're buying them for very steady, slow growth and dividend capture."

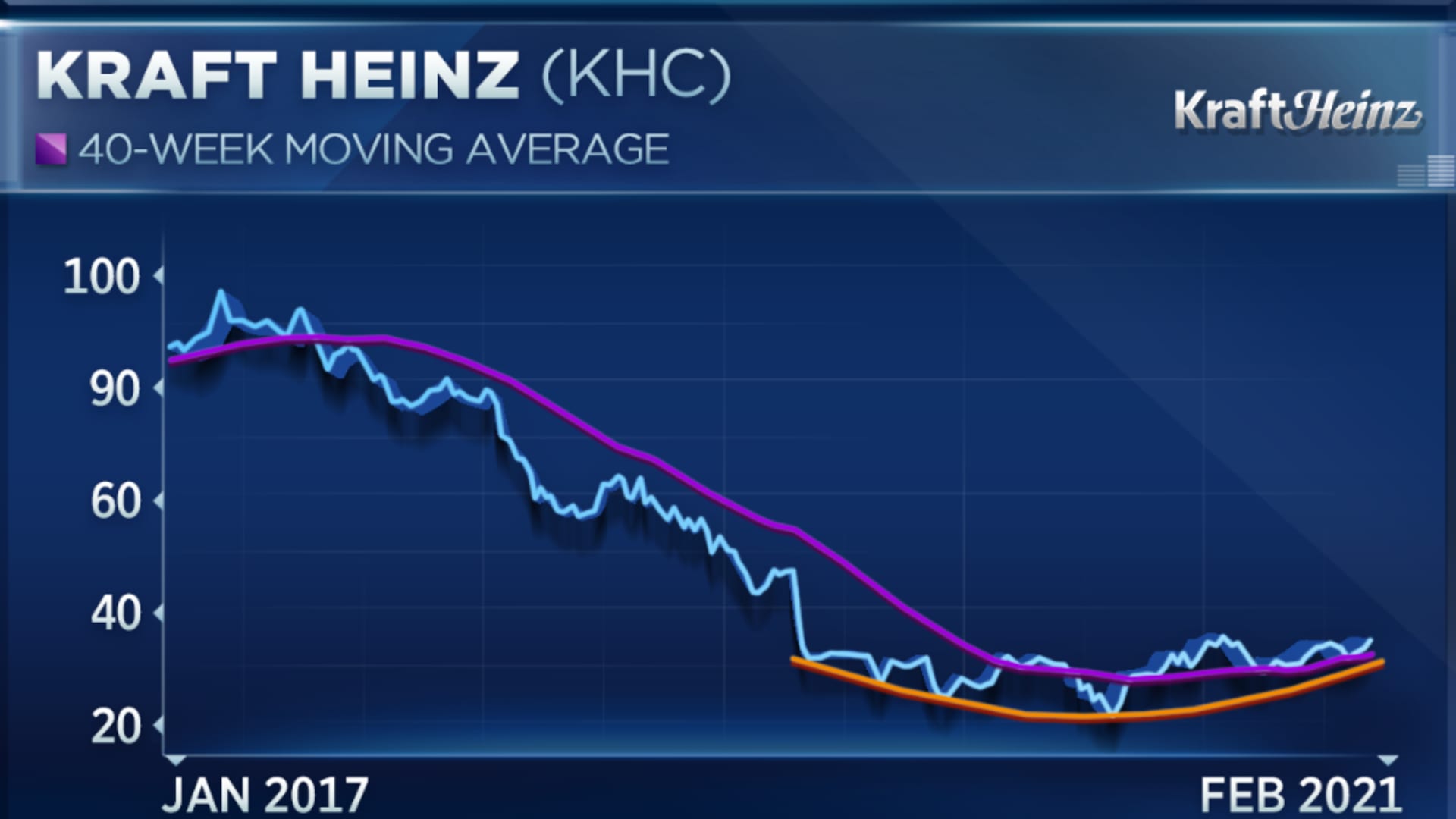

Kraft Heinz's strength is backed up by the technicals, Fairlead Strategies managing partner and founder Katie Stockton said in the same "Trading Nation" interview.

Referencing a chart of the stock, Stockton noted the shares "appear to be advancing from that basing phase that's really been two years in the making."

"Following Boris's comments, the next resistance, assuming that this $36 level is cleared decisively on the back of the earnings report, is about $50," she said. "I think that that's a nice upside target to keep in mind for the stock based on not only the fundamentals, but also the chart."

Kraft Heinz shares ended trading up almost 5% at $35.54 on Thursday.

As for stocks in established uptrends that could keep climbing, Stockton pointed to Procter & Gamble and Walmart, the two largest weightings in the Consumer Staples Select Sector SPDR Fund (XLP), which tracks the overall sector.

"Those names are in solid long-term uptrends and they've seen corrective phases that, to me, make them not only oversold in absolute terms, but of course also relative to the broader market," she said. "They may, indeed, be seen as safe havens if we get into a weaker, broader tape."