- President-elect Joe Biden campaigned on a promise to provide relief on student debt.

- Expectations are for forgiveness around $10,000 per borrower.

- The larger economic benefits of that are debatable, with one prominent study saying adjusting loan payments for income would have more impact.

- Biden could announce his forgiveness plan early in his administration, setting up a battle against congressional Republicans.

If President-elect Joe Biden follows through on his campaign promise to forgive student loans to many borrowers, he'll be checking off an important box for his political constituency.

As a boost to the struggling U.S. economy, however, the move may not have much impact and will draw substantial opposition early in his presidency.

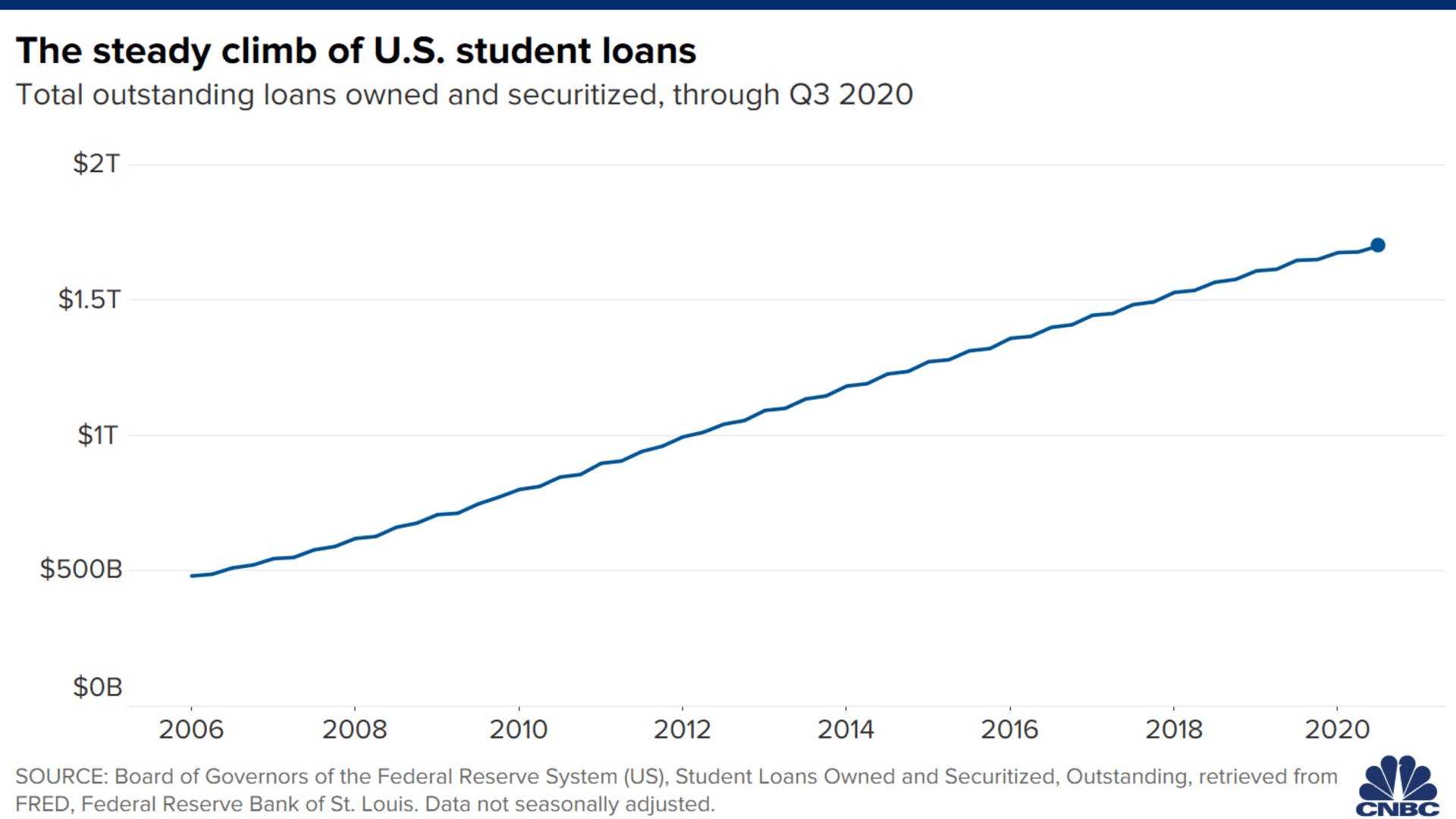

What to do about the burgeoning $1.6 trillion in education debt has been a nagging question for government officials. Fully half of the debt has piled up over the past decade, when effective nationalization of the process opened a floodgate of tuition increases and college loans that left many graduates struggling to pay bills, buy homes and raise families.

The most likely path Biden will follow is a $10,000 forgiveness plan at a time when the average burden per graduate is just shy of $30,000.

That would provide an aggregate savings of more than $400 billion, according to many estimates.

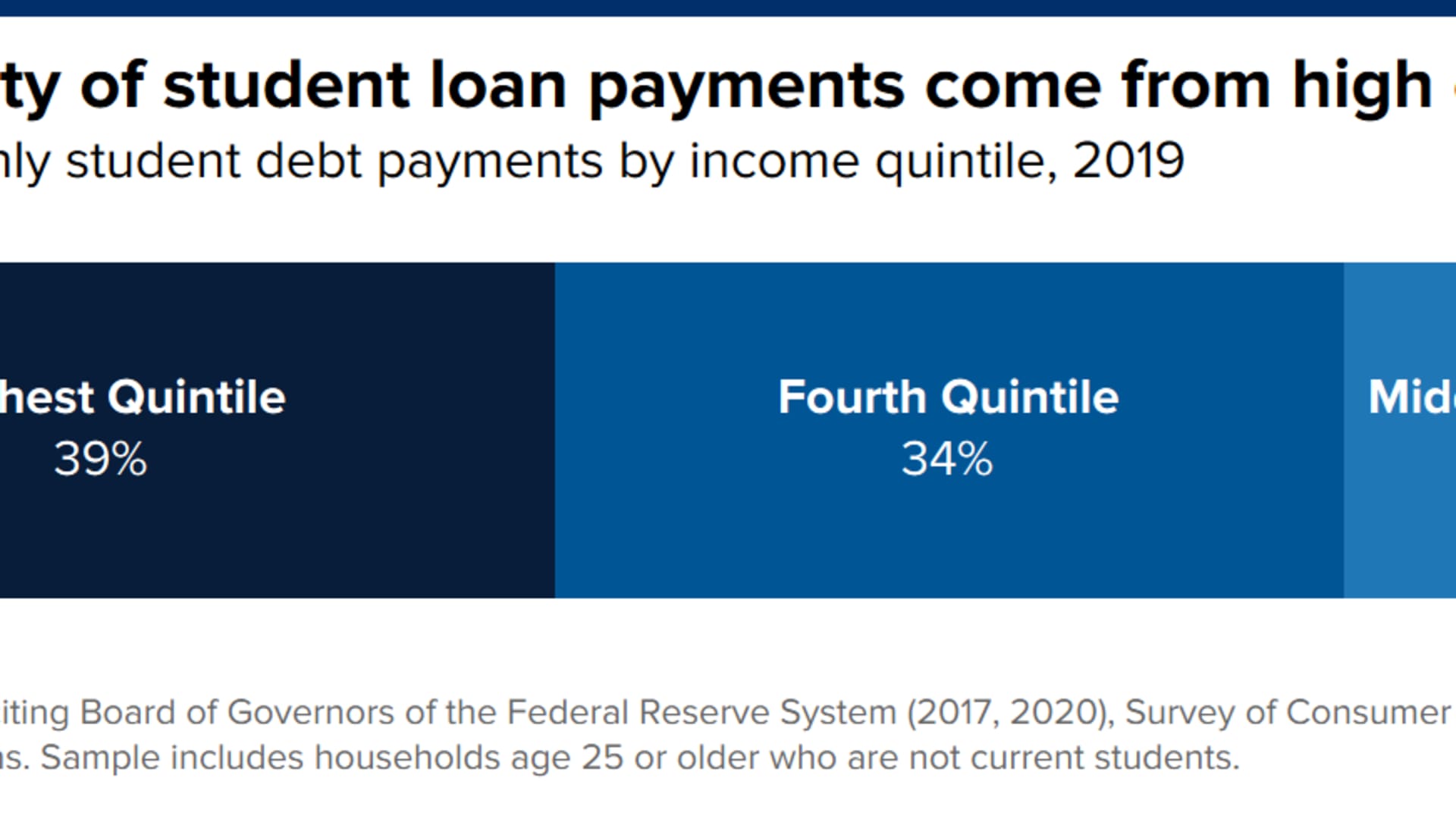

But in doing so, it would raise a series of thorny questions that the new administration may have a hard time answering. Among them are issues over wealth inequality, given that higher-income borrowers owe a larger share, moral hazard of wiping out loans to a select group, and whether forgiveness is even the most effective way to address the issue.

"There is growing evidence that student loan debt does have macroeconomic consequences," said Mark Zandi, chief economist at Moody's Analytics. "Outside of mortgage debt, it's the largest amount of household debt outstanding, and it's still growing rapidly."

Indeed, education loans outstanding totaled just $480 billion at the beginning of 2006. However, two pieces of legislative action that effectively guaranteed access to college, and the funds needed to pay the way, caused that figure to jump 67% over the next four years to $800 billion, and it's more than doubled that total in the decade since.

Studies have linked the burden to lower household formation, higher delinquency rates and lower confidence about the future for borrowers.

Money Report

But whether just wiping the slate clean would really help is an open question.

For his part, even while Zandi insists the idea would benefit the middle class, he sees significant weakness.

"How I would provide relief to hard-pressed student loan borrowers, I think I'd focus more on income-based repayment plans," he said. "If you're really trying to address our long-term education needs, which I think is critical to long-term economic growth, we need to be thinking more expansively about providing higher levels of education at a much lower cost."

Providing outright debt relief, he added, raises the question of, "Do we really want to subsidize tuitions? That's what you're doing. You're giving money to students to give to universities that raised the tuition … and it doesn't really help anybody."

Tying debt to income

The larger efficacy question of loan forgiveness was the study of a working paper released last month by the prestigious University of Chicago Booth School of Business.

Researchers Sylvain Catherine, of the University of Pennsylvania's Wharton School of Business, and Constantine Yannelis, from the Booth school, compared the benefits of forgiveness against those of income-based payment plans that Zandi mentioned. They found the latter provided better benefit, particularly for lower-income borrowers.

Those with higher debt loads, the study found, tend to be students in post-graduate programs who also are making more money. Thus, they would benefit more from forgiveness and widen a growing disparity among income classes in the U.S.

"We find that universal and capped forgiveness policies are highly regressive, with the vast majority of benefits accruing to high-income individuals," the authors said. "On the other hand, enrolling more borrowers in [Income-Driven Repayment] plans linking repayment to earnings leads to forgiveness for borrowers in the middle of the income-distribution."

Current IDR plans, as they are known, would have payments pegged at 10%-15% of discretionary income for borrowers with incomes 150% above the poverty line. Any remaining balances would be forgiven after 20-25 years. The provisions mean that low-income debt holders still might end up paying nothing or very little over the lives of their loans.

"Forgiveness would benefit the top decile as much as the bottom three deciles combined," Catherine and Yannelis wrote. "Blacks and Hispanics would also benefit substantially less than balances suggest. Enrolling households who would benefit from income-driven repayment is the least expensive and most progressive policy we consider."

Political questions

Selling those types of economics, though, could be tough at a time when debt holders and progressive politicians on Biden's side of the aisle are demanding immediate relief.

The president-elect made such populist themes as easing the student loan burden a centerpiece of his campaign and he will be pushed to come through, with some members of his party advocating forgiveness as high as $50,000.

Following through, "will be transformational and provide a boost to Biden's approval among the borrowers who will benefit, further cementing educated millennials and other post-generation X age cohorts into the Democratic coalition," Beacon Research said in a recent policy note on the issue.

Beacon said it expects the issue to be part of Biden's first-100-days agenda.

But opposition is likely to be substantial, providing an early faceoff for the new president and Republican lawmakers who could still control the Senate.

The Committee for a Responsible Budget, fearing more kindling on the nation's $27.4 trillion debt, said the $115 billion to $260 billion economic benefit would yield "a much smaller return than other options available to policymakers."

The organization said government spending would be more beneficial in the form of direct payments like extended unemployment benefits, which are part of stimulus packages being bandied about in Congress.

There also will be general political backlash on moral hazard grounds from those who see folly in rewarding students for racking up huge debts they couldn't afford to colleges that took advantage of government largesse to jack up costs.

Government has "allowed universities to go on this crazy trajectory of increasing their costs without any additional benefit to students," said Carol Roth, head of Intercap Merchant Partners.

"Colleges bear a lot of the responsibility, and they have basically been taking the dollars facilitated by government in a predatory way," she added.

While Roth acknowledges the larger economic issues, she said it's wrong that taxpayers have to pick up the tab for some borrowers and not others.

"We have to move away from governments picking winners and losers," she said. "The government shouldn't be doing that, and it's not fair to have people who decided not to go to college, whether it's directly or indirectly, bearing the burden for the situation they had no role in causing."