- Roughly 1 in 3 households had trouble making ends meet right before the coronavirus pandemic.

- By September, nearly 5 million more people were living in poverty than before the pandemic, according to one study.

- Some groups, like minorities, low earners, women and those without college degrees, have suffered the most, according to financial experts.

Vicki Honeycutt lost her job in March, one of millions laid off in the early days of the coronavirus pandemic. To make matters worse, Honeycutt, an executive assistant at a bank, had no savings.

Biweekly paychecks of around $1,600, after taxes, were devoted almost entirely to bills, including $1,100 in rent and medical expenses for her daughter, who has a rare autoimmune disorder. Honeycutt's husband, James, is a veteran with a disability that makes it difficult for him to work.

"I was always finagling, and we didn't have anything left over," Honeycutt, 53, said.

Over the last few months, she's applied to more than 100 jobs but nothing has panned out. She and her family are now being evicted from their house in China Grove, North Carolina, where they've lived for 10 years.

More from Personal Finance:

Here are the top 5 U.S. cities for retirement

Three things to keep in mind to handle market volatility

These hidden fees take bite out of retirement savings

"My husband and I used to kid around and say, 'We're just a paycheck away from being homeless,'" Honeycutt said. "Our worst nightmare came true."

Money Report

Even before the coronavirus pandemic, a large share of Americans lived paycheck to paycheck, teetering precariously on the edge of financial ruin.

Years of stagnant wages, especially among low-income earners and people of color, coupled with the rising cost of living, made it harder and harder for many people to put much if any of their earnings away in case of an emergency, let alone for goals like buying a house, sending their children to college or preparing for their old age.

One in 3 households reported difficulty making ends meet in January, before the onset of the economic and health crises, according to a recent Harvard University, George Washington University and University of Oxford study. Some 40% of Americans said they couldn't cover a $400 unexpected bill without selling something or going into debt, a 2018 Federal Reserve report found.

In other words, even as the country was in the midst of its longest economic expansion in history and unemployment levels were at half-century lows, families were one home repair, medical bill or lost paycheck away from potential disaster. Then a disaster of epic proportions hit: the Covid-19 recession.

"What we're seeing now is things getting considerably worse," said Peter Tufano, dean of Oxford's Saïd Business School.

That deteriorating financial condition is largely a result of mass joblessness and the absence of an adequate federal support system to prop up lost wages in recent months, according to economists.

This wasn't the case in the early months of the Covid-19 recession.

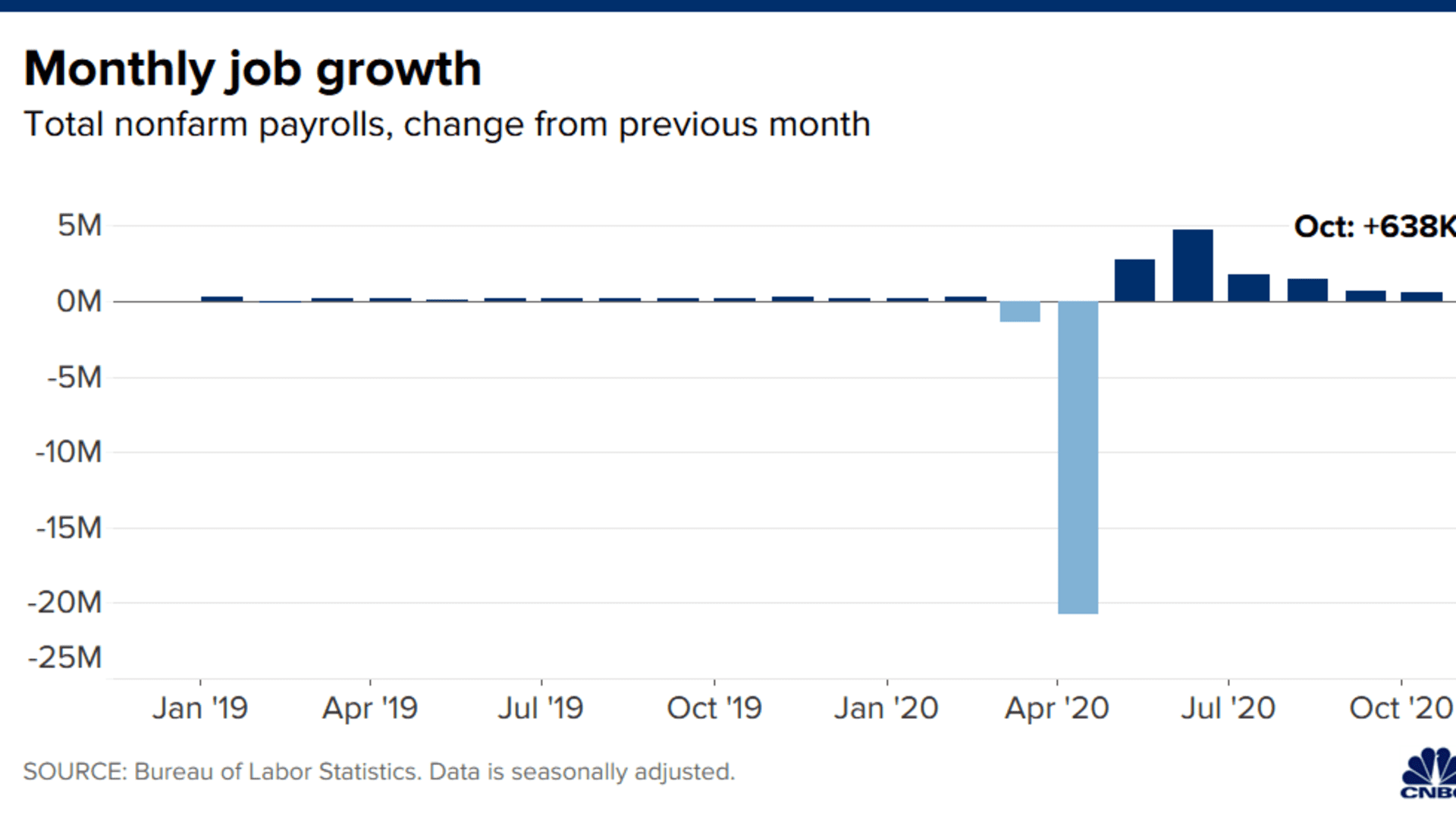

In March, Congress swiftly passed a $2.2 trillion federal relief package, the largest in U.S. history, to combat the economic downturn. That law, known as the CARES Act, established measures to increase unemployment benefits by $600 a week, make aid available to more workers like the self-employed, and send one-time stimulus checks of up to $1,200 to individuals.

In all, the stimulus package helped lift 18 million Americans out of poverty in April, according to Columbia University researchers.

But financial distress grew throughout the summer as households spent their stimulus checks and after the $600 unemployment benefit lapsed in July. By September, 4.6 million more people were living in poverty than before the pandemic, according to the Columbia study.

Making everything worse is the fact that so many Americans had little to no savings to fall back on.

"If we think about the various lines of [financial] defense, the most important one by a long stretch is savings," Tufano said.

'No way to prepare'

In 2011, Michelle Kulaski began working at Pier 1 Imports, a home goods retailer, in Fayetteville, Arkansas. She was promoted several times over the years, eventually becoming assistant manager. Even then, Kulaski made just $15 an hour. Rent, car insurance and other monthly bills swallowed her entire paycheck.

Kulaski's life became harder when she developed a severe case of carpal tunnel syndrome from moving heavy furniture all day. She eventually needed several surgeries and wasn't able to work as many hours a week.

"There was no way to prepare for an emergency," Kulaski, 50, said.

Then, Pier 1 was forced to shut its stores for good, another business casualty of the pandemic. Kulaski lost her job.

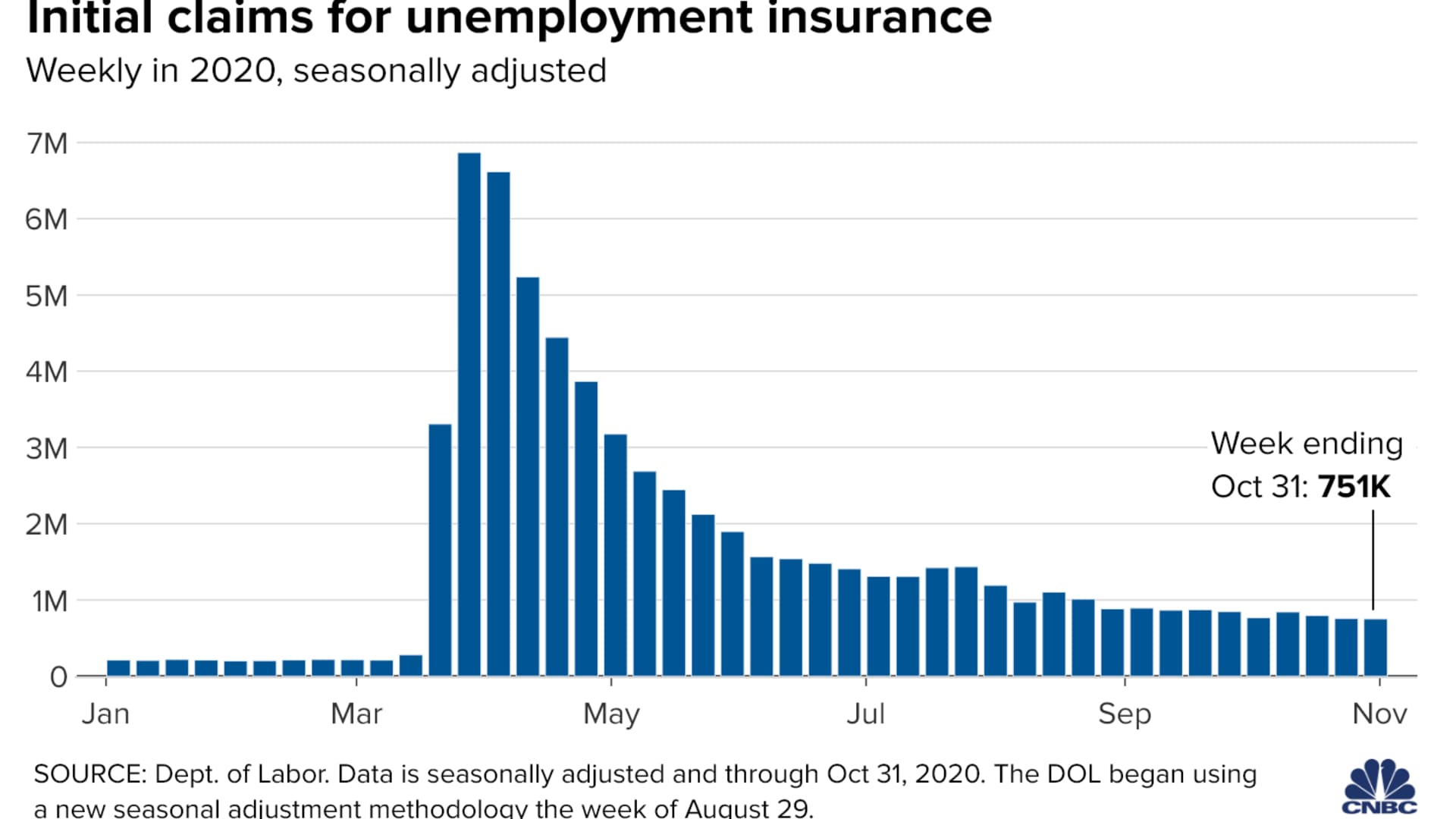

More than 17 million Americans had hurtled into unemployment by the peak of the economic crisis in early spring. Even after six months of declining unemployment, nearly 6 million more people remain jobless than before the recession.

In addition, nearly 7 million people are being forced to work part-time, despite wanting a full-time job, due to current economic conditions, according to the Bureau of Labor Statistics. Meanwhile, the unemployed outnumber job openings by a 2-to-1 margin, making new work hard to come by.

Kulaski has applied to dozens of jobs since she was laid off, to no avail. Instead, she found a part-time position working on product displays for Walmart. She makes around $14 an hour but has no set schedule. In the last week of October, she was only asked to work for nine hours.

"It's super scary," Kulaski said. "I know I need that money and without it, I'm going to get further behind."

Many Americans are in a similar bind.

In August alone, the month after the $600 unemployment boost ended, jobless workers spent two-thirds of all the savings they'd accumulated from those extra benefits, according to JPMorgan. Around half of Americans say their No. 1 financial priority of late is "staying current on bills," up from 38% last year, according to a recent Bankrate.com survey.

"Given the lack of employment, the likelihood of people living paycheck to paycheck is increasing," according to Till von Wachter, an economics professor at the University of California Los Angeles and director of the California Policy Lab.

'Man-made' crisis

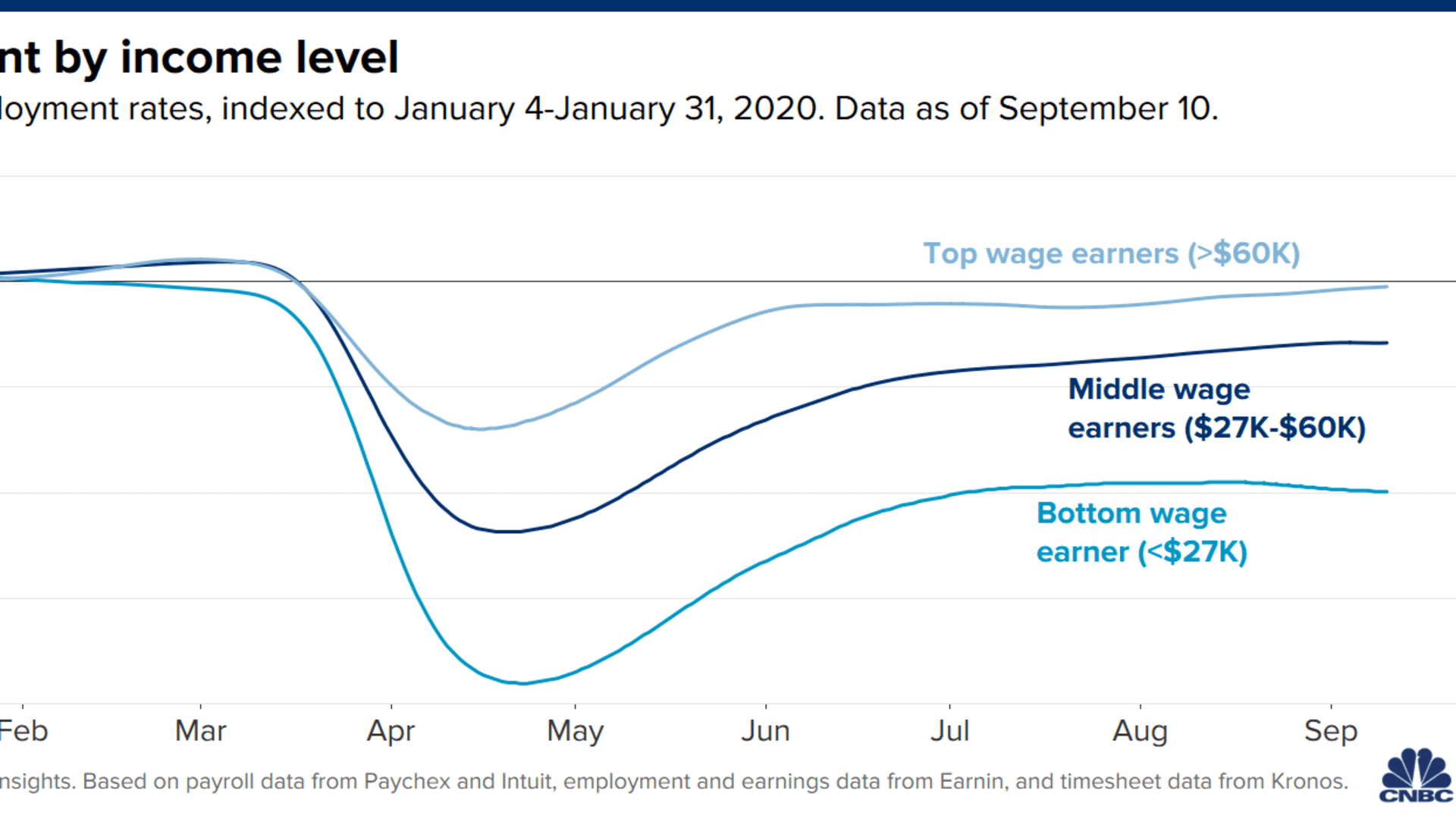

While no segment of society escaped the initial economic shocks of the Covid-19 recession, the pain has been concentrated among certain groups like lower earners, minorities, workers with less education and women.

Such individuals disproportionately work in industries such as hospitality and food services, which experienced a large share of the job loss caused by Covid-19, and are generally more likely to be living paycheck to paycheck, according to economists.

They've also been among the last to return to work. For example, jobs for people making less than $27,000 a year are still 20% below their levels in January, while those making at least $60,000 a year have fully recovered their lost jobs, according to Opportunity Insights.

The recession has placed severe financial stress on the households least likely to be able to weather it.

"We created these fragilities over decades, in terms of setting policies and organizing our economy in a way to create incredible income inequality," said Wendy Edelberg, director of the Hamilton Project at the Brookings Institution, a left-leaning think tank, and former chief economist at the Congressional Budget Office. "Much of this crisis is man-made."

That's partly a result of anemic wage growth, which has stagnated for decades especially among lower earners, according to von Wachter.

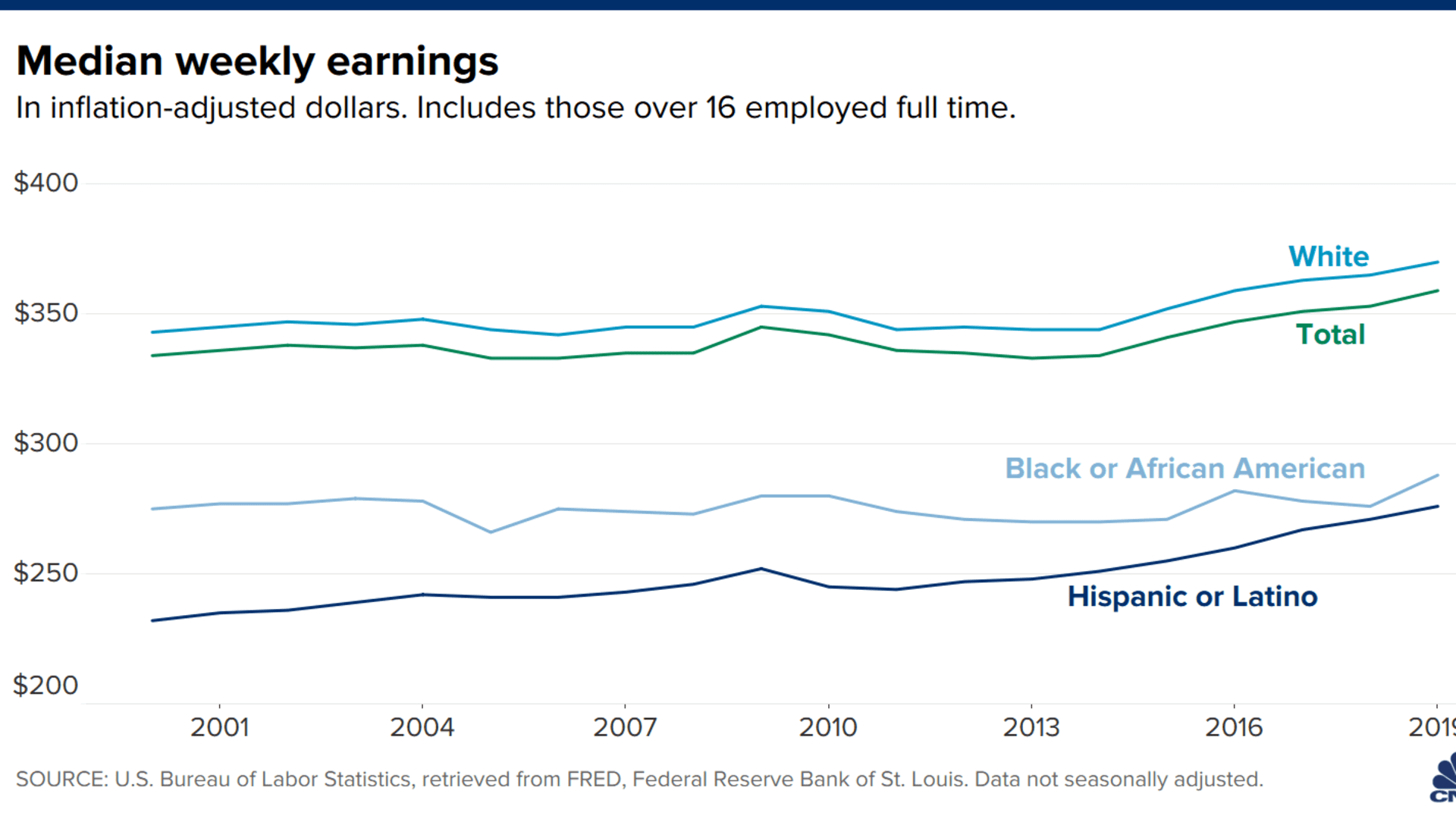

The typical full-time American worker made $359 per week in 2019 after adjusting for inflation, according to the Federal Reserve Bank of St. Louis. That's just 8% higher than the $332 weekly pay four decades ago.

Black workers have seen their incomes rise at about half the rate of White workers, according to Federal Reserve data.

The value of the federal minimum wage, which hasn't budged from $7.25 an hour since 2009, has eroded over time. Nearly half of states use this as their prevailing wage for workers, according to the National Conference of State Legislatures. (Other states, as well as cities, set a higher threshold.)

Individuals working minimum-wage jobs have lost nearly 10% of their buying power due to inflation over the past decade, according to the Pew Research Center.

"This is hitting people who have the fewest resources," Edelberg said.

Meanwhile, the cost of living has swelled.

Rent, for example, has placed cost burdens on a growing share of households. In 2016, the typical renter among the bottom 25% of wage earners had just $488 a month to spend on other essentials like food, utilities and transportation, after paying rent.

'It doesn't matter how hard you work'

Without savings to lean on in difficult times, workers risk falling behind on debt and rent payments and relying on predatory relief valves like high-interest payday loans.

Americans had a 1 in 3 chance of missing a rent or mortgage payment in July, according to the World Bank. At one point, it was estimated that as many as 40 million Americans could face eviction in the public health crisis.

After Kulaski lost her job, one bad thing happened after the next.

First, her car was almost repossessed because she couldn't come up with the $236 monthly payment. Without a car, she wouldn't have a way to get to work or the grocery store. Fortunately, she reached an agreement with her lender.

However, she's been forced to max out her credit cards and was dinged with multiple overdraft fees from her bank. The average charge during the pandemic is more than $33, the highest it's been in decades, according to Bankrate.com.

Desperate for cash, Kulaski sold much of her furniture, including the bed her children sleep in when they visit and her grandparents' desk. In all, she made around $300.

Still, Kulaski has fallen behind on her $755 rent and her landlord has moved to evict her.

If she has to leave her apartment, she said she'd probably live in her car with her two cats.

"It's devastating," she said. "It doesn't matter how hard you work; I was doing everything I could to be independent and take care of myself."

Uncertain paychecks

It can also be harder to save money when a person's income is unpredictable.

Jennifer Ochsner was juggling three jobs before the pandemic hit. She worked at a gym, at a bar and as an office manager at a psychology practice. Even so, her income mostly just kept her afloat.

"It covered everything but there wasn't much extra," said Ochsner, 29, who lives in Colorado.

And then the recession claimed two of her three jobs, leaving her with just 12 hours of work a week.

"My checking account was going down throughout those months," she said.

Ochsner was recalled to work at the gym — her main gig — last month, just in time to pay her November bills.

More than 8 million Americans, like Ochsner, held more than one job last year, according to the Bureau of Labor Statistics. Women are more likely to do so than men. Research has also found that most of the new jobs created over the last decade were considered "alternative work," including freelance gigs and temporary positions.

Amanda Collins had been unable to secure full-time, permanent work after the Great Recession. Instead, she bounced around from one temporary contract I.T. position to the next.

"There was never a sense of security," Collins, 39, said. "I told my friends I was a professional job hunter."

Whenever she built up a little savings, she'd then run through it during the gaps between her contract jobs. She had less than $1,000 in the bank.

Then, a breakthrough: In 2018, she was hired as a service desk analyst at the Kennedy Center for the Performing Arts in Washington, D.C. For the first time in a decade, she was a salaried employee with benefits like paid vacation time, health insurance and a retirement plan.

"It was fantastic," Collins said. "When you get a permanent job you can try to plan." And she did: She was saving up and hoping to one day buy a condo in D.C. "It would be nice to have a place of my own," Collins said.

But now she's had to shelve those plans. She was furloughed in March, and then laid off in July.

She's applied to 20 or so jobs, but is still unemployed. "I've started getting calls from recruiters but it is often much less pay," she said, adding that she expects to have to take another temporary position again.

In the meantime, she's borrowed money from family to keep up with her bills, and may have to go into debt.

"My credit cards are my safety net right now," Collins said.