- Anyone who's nearing retirement may want to make sure their investment portfolio is constructed in a way that mitigates "sequence of returns" risk.

- The goal is to avoid being forced to sell investments for cash-flow needs if you retire in a down market.

- While it's uncertain where stocks will go from here, volatility in prices is expected to continue.

If the stock market's volatility is worrying you because you're edging closer to retirement, it may be time to reevaluate your portfolio.

One of the big risks you can face as a new retiree is a persisting market downturn just as you need to start tapping your savings. Because research shows the long-term harm this can cause to your portfolio, it's worth heading into retirement with your money allocated in a way that mitigates that risk.

"One of the things that I've seen too much of ... is retirees being invested way too aggressively early in retirement," said certified financial planner Carolyn McClanahan, founder of Life Planning Partners in Jacksonville, Florida.

Feeling out of the loop? We'll catch you up on the Chicago news you need to know. Sign up for the weekly Chicago Catch-Up newsletter here.

With the Russia-Ukraine conflict adding uncertainty to an already sliding market, the major indexes have continued zigzagging their way through the pullback. Year to date, the S&P 500 Index — a broad measure of how U.S. companies are faring — is down 8.8% through Monday's close. The Dow Jones Industrial Average is off roughly 7% so far this year, and the tech-laden Nasdaq Composite index has slid 13%.

The math looks better over the longer term, however: The S&P is up more than 12% over the last 12 months, the Dow is up nearly 7.5%, and the Nasdaq's one-year return is about 1.2%. While it's impossible to predict where the market will go from here, volatility is expected to continue.

Money Report

For long-term savers — those whose retirement is many years or decades away — the ups and downs of the stock market generally matter less because their portfolios have time to recover before being relied on for cash flow.

It's a different story in retirement. And for those just beginning that chapter of life, this can be an especially acute problem.

Essentially, research has shown that a "sequence of returns" risk can cause a long-lasting negative impact to your portfolio. This risk basically is about how the order, or sequence, of your losses or gains over time matters when you are liquidating investments.

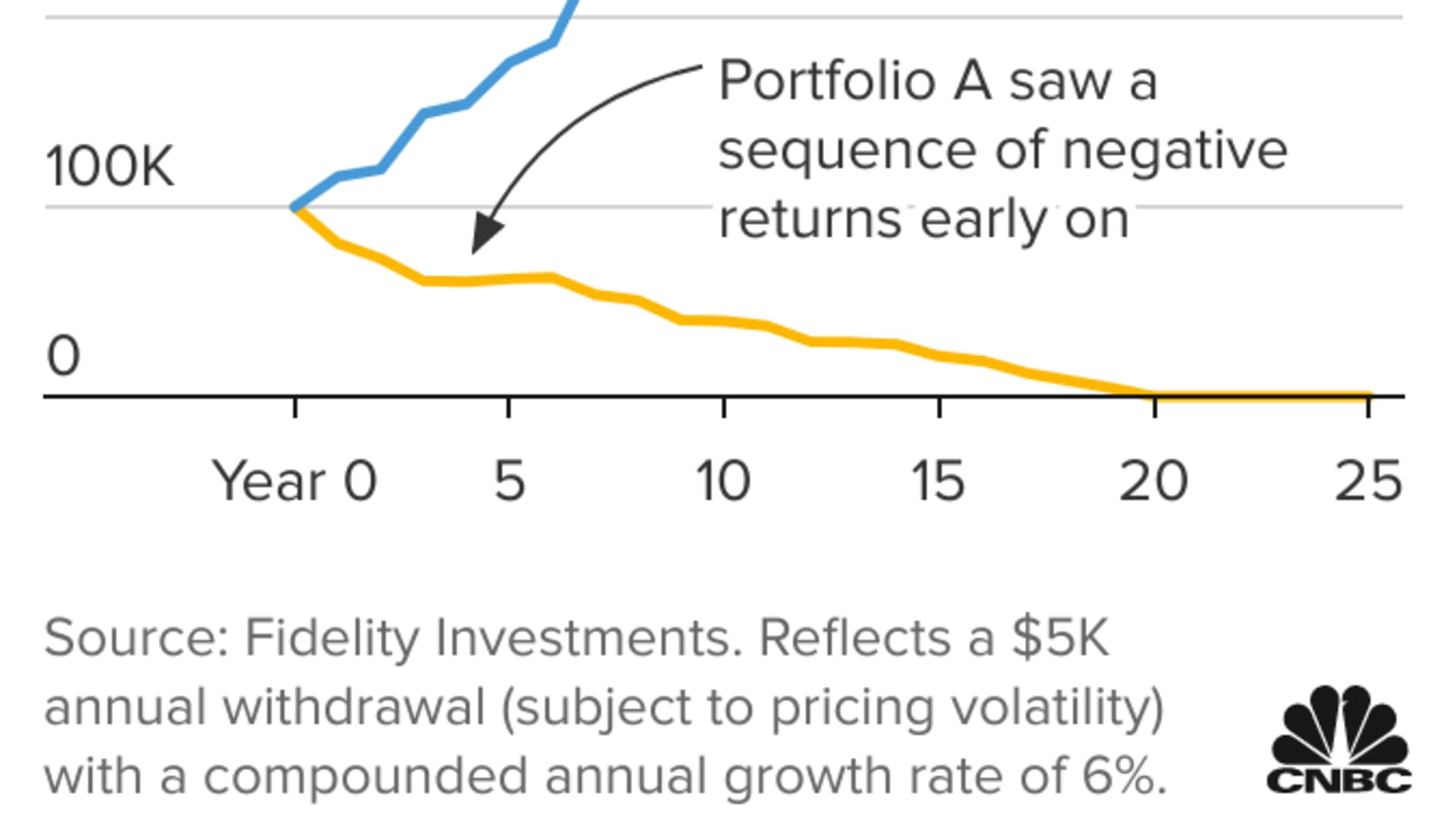

The chart below illustrates the difference that market losses versus market gains early in retirement can have. In the chart, both portfolios hold the same investments and experience the same annual returns, but in opposite orders over 25 years.

Both hypothetical portfolios start with $100,000 and experience $5,000 annual withdrawals, but Portfolio A begins with a sequence of negative returns and Portfolio B has those losses at the end of 25 years. The difference is stark: Portfolio A is depleted by year 20 and Portfolio B ends up with more than double the assets that it started with.

"It's really important for today's retirees and pre-retirees to understand [that risk] to their nest egg," said Vance Barse, wealth strategist and founder of Your Dedicated Fiduciary, which has offices in San Diego and Prosper, Texas.

If your planned retirement date is approaching, it's worth checking to see if your portfolio is constructed in a way that addresses this sequencing risk. Generally speaking, this means trying to keep any money you'll need to meet your expenses away from stocks and other riskier investments.

Some advisors recommend having one or two years' worth of cash or cash equivalents on hand to avoid selling into a down market.

"Make sure you have enough cash so you don't have to sell your [investments] to have cash," said David Peterson, head of wealth planning at Fidelity Investments. "You don't want to do that in a down market."

Part of knowing how much cash you will truly need means having a good grasp on both your other sources of income — i.e., Social Security, pension, annuities — and your actual spending.

"Many people inadvertently minimize their expenses," Barse said.

Beyond having cash, it's worth ensuring that the rest of your assets aren't too heavily invested in stocks.

McClanahan said her retired clients maintain five years' worth of conservative investments to meet cash-flow needs.

"That way they don't need to wait until a crappy market to figure this out," McClanahan said.

She said that for new retirees whose savings is just enough — i.e., there's not a lot of room for error — a conservative portfolio composed of 50% stocks and 50% bonds may be appropriate.

"But we have some clients that are only 30% or 40% in stocks," McClanahan said. "It's about how much risk you can take financially and psychologically."