- A tax refund offers a rare opportunity to give your long-term financial standing a boost.

- Here are three ways to stretch the one-time payment.

The IRS has already issued more than 45 million refunds this year, at an average $3,352 each.

That's over $500 more than last year, when the average refund was just over $2,800.

For most Americans, a lump-sum payment of this size is rare and fewer people want to squander it.

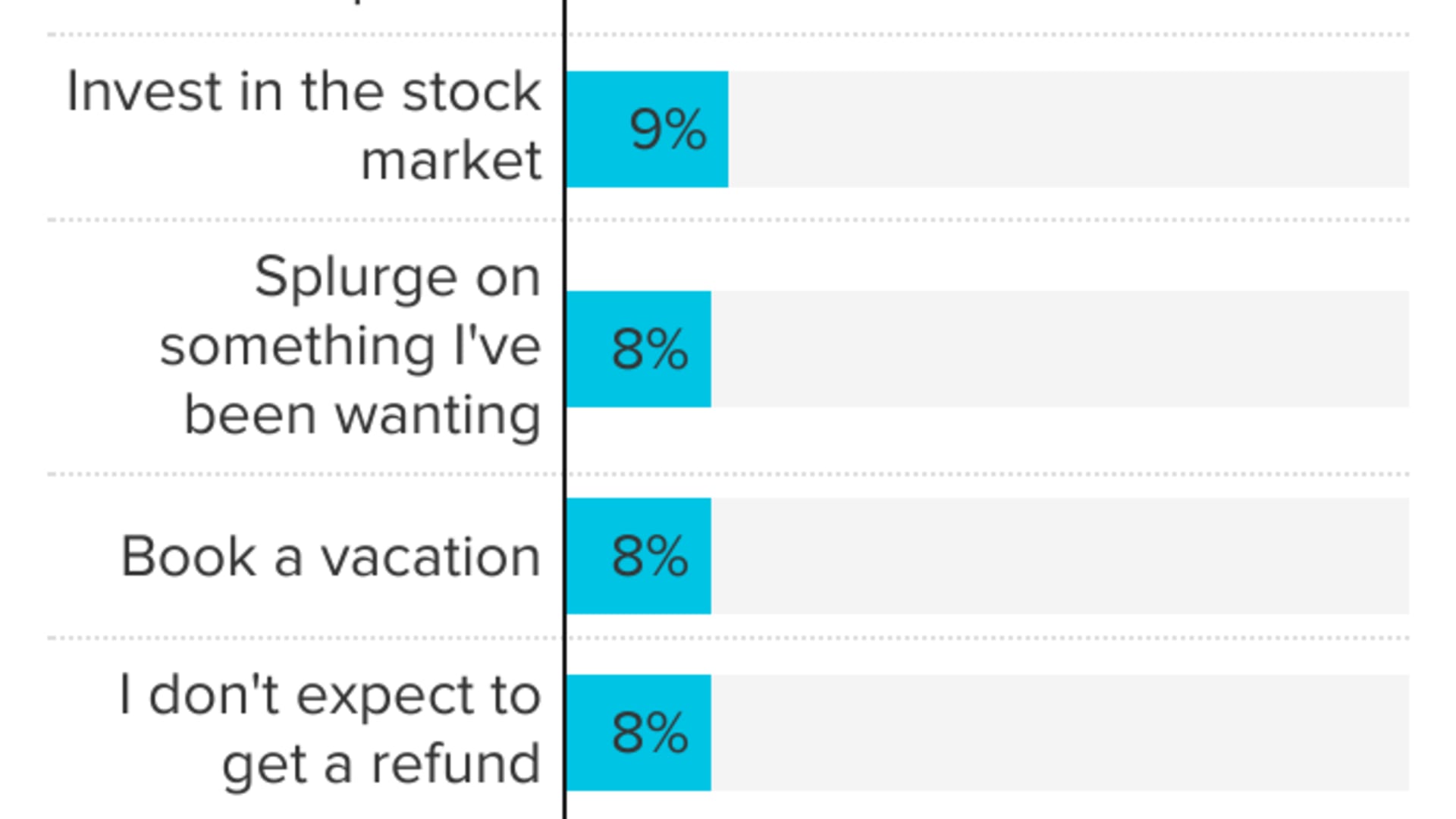

Now, nearly half — or 46% — of tax filers plan to save their refunds, according to a LendingTree survey, up from 41% last year and 40% in 2020.

"The tax refund is often the biggest windfall households receive all year," said Greg McBride, chief financial analyst at Bankrate.com.

Money Report

In order to make the most of that money, experts recommend focusing on the long-term, particularly if you've been been hit hard by the pandemic.

Here are three ways to invest your tax refund in your future:

1. Build up your emergency savings

More than one-third, or 34%, of households have less in emergency savings now than they did before the pandemic, according to Bankrate.com.

"Households that have experienced income disruption during the pandemic are very likely to need to rebuild their emergency savings," McBride said.

More from Personal Finance:

There are just weeks until the tax deadline

Here's why your tax return may be flagged by the IRS

Here's what every taxpayer needs to know this season

Most financial experts recommend stashing away at least a six-month cushion — or more if you are the sole breadwinner in your family or in business for yourself.

Direct depositing that tax refund into an emergency savings account is a great way to take a significant step forward financially and give yourself a much-needed cushion for whatever lies ahead, McBride said.

2. 'Turbocharge' your retirement

If you've established a solid emergency fund, then consider your retirement savings, advised Rita Assaf, vice president of retirement leadership at Fidelity Investments.

"This is a great way to turbocharge your savings," she said.

Assaf recommends contributing at least enough to your workplace retirement account to take full advantage of the employer match or, if possible, the maximum amount workers under 50 can put in, which is now $20,500 in 2022.

if you can afford even more, Assaf recommends contributing to both a 401(k) and an individual retirement account. You can set up direct deposit into either a traditional IRA or Roth IRA account and contribute up to $6,000 in total. (Generally, traditional IRAs are most effective if you expect to be in a lower tax bracket when you retire, while Roth IRAs are best for those in a lower tax bracket today.)

Another option is to purchase federal I bonds, which are inflation-protected and nearly risk-free assets, paying a 7.12% annual rate through April. As the cost of living spikes, this will work well as a hedge against inflation for long-term savers — the downside is that you can't redeem I bonds for one year, and you'll pay the last three months of interest if cashed in before five years.

3. Plan for your children's future

"If your family is financially able to do so, leveraging a tax refund to jumpstart education or disability savings is a great opportunity to support long-term goals," said Mary Morris, CEO of Virginia529 and ABLEnow.

Many 529 college savings plans offer tax benefits that are better than using a simple savings account.

Not only can you get a tax deduction or credit for contributions (currently 34 states and the District of Columbia offer a direct state tax deduction for your contributions), earnings grow on a tax-advantaged basis and, when you withdraw the money, it is tax-free if the funds are used for qualified education expenses such as tuition, fees, books, and room and board.

Generally, you will need to have opened an account first but with many plans you start with as little as $10, Morris said. That "money can grow free from federal taxes, and an upfront lump-sum contribution may benefit from potential market gains," she added.

Similarly, you can set up to $16,000 aside in an ABLE account, which is another tax-advantaged savings plan, also administered by individual states, for people with disabilities and their families.

The money in ABLE accounts grows and can be withdrawn tax-free and the funds can be used for a variety of expenses, from housing to long-term health care, all without any limitations on the number of withdrawals.

Using your tax refund to put a few hundred — or thousand — dollars in into one of these accounts could be "a real game changer for families that have not been able to save or plan for the future," Morris said.